Investing in nature means prioritizing health & resilience

As nature-loss, mass extinction, ecosystem breakdown, and climate disruption impose more and more serious impacts, there is growing awareness that we need to invest in nature. The idea is controversial, though, because historically, investing in nature has meant either exploiting (and destroying) nature or turning nature into a commodity, which often ends up being the same thing.

In 2023, 31 years after The Rio Conventions—in which nearly 200 countries agreed to prevent dangerous climate change, protect biodiversity, and roll back desertification—we find ourselves facing polycrisis. The effects of climate disruption, nature loss, which likely triggered the COVID-19 pandemic, rapidly rising costs of disaster response and rebuilding, a sovereign debt crisis, and the corrosive impacts of conflict and food insecurity, have created a compounding mess, which no nation will easily overcome.

Since 1992, when the world effectively agreed to work together to stop environmental destruction, we have not invested in nature at the scale required to achieve a sustainable future for humankind. We have focused mostly on marginal experiments:

conservation credits, which come with ongoing pollution;

small direct subsidies for sustainable practices that are dwarfed by the subsidies going to unsustainable practices;

biofuels which are supposed to create a “net” benefit, but which still pollute and also consume much-needed agricultural land;

circular economy experiments even include an astounding approval for Chevron to make fuel from plastic.

We need far, far more, and better. Green bonds, and other sustainable impact bonds, are an important example of leadership. Green bond issuance has risen from $40 billion in 2015—when the Paris Agreement, the Sustainable Development Goals, and the agreements on Financing for Development and Disaster Risk Reduction, were agreed—to $443 billion in 2022. The pace in 2023 is a bit faster; estimates are new green bond issuance could reach $600 billion this year.

These are promising trends, but policy and market behavior have yet to adjust to the logic underlying them: all money needs to become climate-smart, resilience-building, and inclusive of those too long excluded from the capacity acceleration that is the core logic of finance, as such.

The Glasgow Financial Alliance for Net Zero brought together 450 financial institutions, in November 2021, committing to align $130 trillion—1/3 of all financial wealth—with science-based net-zero targets.

Much of that realignment has not yet started, let alone become a mainstream operating principle at these institutions. There is too much wait-and-see thinking still governing decisions.

As the ‘integrated and holistic’ approach called for by the Paris Agreement gathers momentum, we need policies and instruments that support economy-wide mainstreaming of sustainable finance.

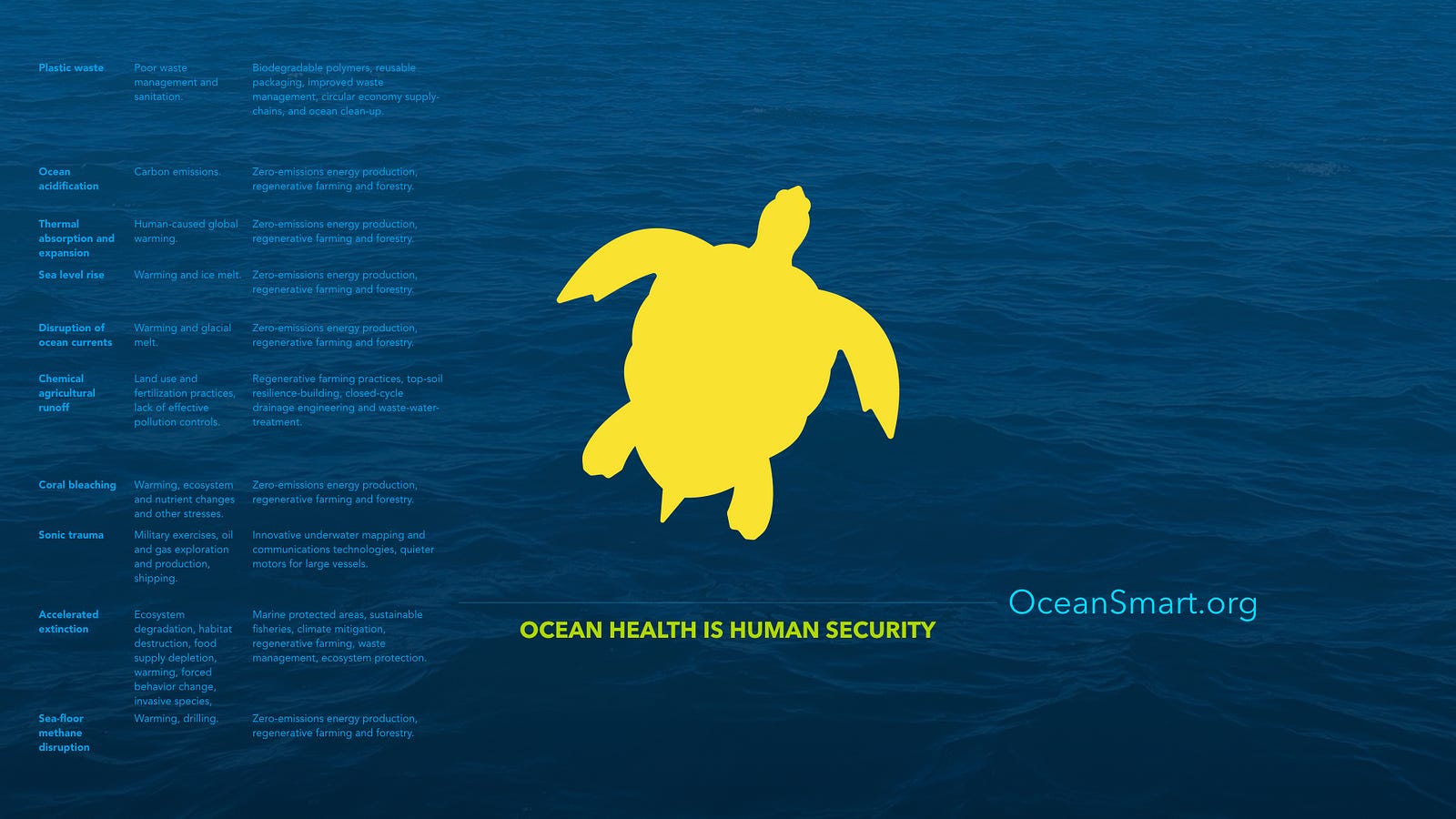

The 2019 Invest at the Source report, from a high-level dialogue on ocean sustainability, identified upstream investment in ocean health as a critical blue-economy priority. Agriculture, for instance, can stop chemical runoff that pollutes waterways, degrades ecosystems, and leads to hypoxic ‘dead zones’ offshore. The same is true for the chemical industry, the energy sector, infrastructure and urbanization, and mineral extraction.

Non-target sectors can support critical science-based targets that give us operational compliance with climate and sustainable development goals. The ‘blue economy’ can be, and should be, the ocean-smart economy. Climate investments should be climate-smart investments in all areas of human activity—not only in a short list of climate solutions. Investments in nature need to be nature-positive and economy-wide as well.

This means there is space for the creation of instruments and strategies that act on financial needs and priorities not related to nature:

instruments that allow for bundling segments of mainstream investments into pools of funds that support nature-positive action;

insurance products linked to resilience-building and sustainable diversification, which can be supported by fiscal policy measures;

intermediary data services that enhance overall bankability of efforts to restore ecosystems, reduce pollution, and improve human health;

innovative technologies that can serve as delivery mechanisms for direct incentives to unbanked and underserved local actors.

The critical missing insight, in much of the policy and finance discussion, is that the health of natural systems is a critical driver of human health, wellbeing, and sustainable prosperity. Investing in nature means investing in people—in human health, in sustainable opportunity, and in the prospects for a better future all around.

We don’t need to commodify nature, ecosystems, and biodiversity in order to make investments in nature into market-making incentives. Instead, we need incentives that operate at multiple scales to encourage new practices and business strategies that don’t harm nature in the first place.

Good Food Finance Week 2023