Compounding climate pressures will force the greening of capital

Climate stress, compounding costs & the greening of capital, are all picking up speed. Every actor, in every sector, needs to join the Race to Zero.

As global average temperatures continue to rise, due to still expanding carbon pollution, the risk, cost, and impacts of climate disruption are getting worse. More regions are now seeing regular, various, and overlapping climate disruption impacts—including summer and winter storms, drought and flooding, degradation of ecosystems, and firestorms big enough to make their own weather.

Some of these impacts are clearly already compounding each other’s effects. That we can see compounding climate impacts so visibly, in direct human experience, now, at roughly 1.2ºC of global heating, means we will be seeing far higher climate emergency costs even in the best case scenario.

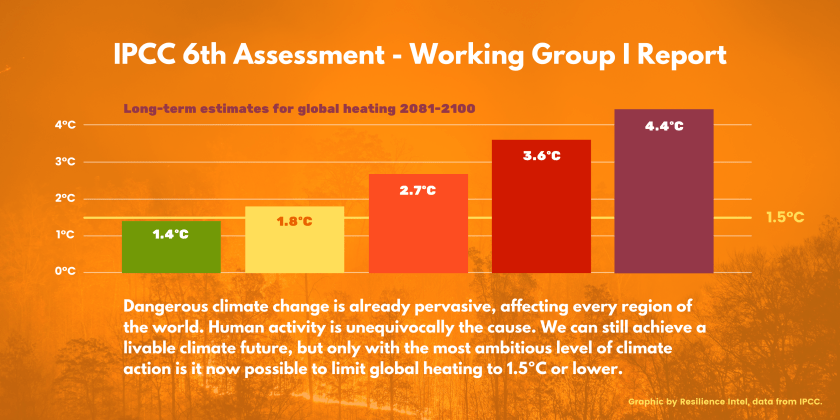

In its landmark August 2020 report on the physical science basis for the 6th Assessment, the Intergovernmental Panel on Climate Change examined all historical observations and projected 5 possible futures, based on the best scientific evidence.

Of the 5 futures examined, only the one in which the world’s nations and industries successfully execute high ambition climate policy and innovation everywhere, sustainably, starting right now, can we limit global heating to 1.5ºC or less in the year 2100. Even in that best-case scenario, we will breach 1.5ºC before nature draws down enough heat-trapping gases to bring us below 1.5ºC.

We are seeing compounding effects now. Destabilization of the climate system will continue to add to this compounding effect. 1.6ºC won’t be 33% worse than 1.2ºC, but potentially several times worse in terms of harm and cost.

We should expect entire “breadbasket” regions will fail—possibly beyond just annual crop failure, but suffering ongoing, deep degradation—putting the global food supply at risk. We should expect mass migration on a scale not previously seen, and the failure of nation states, including some not considered now to be at risk of political or economic collapse.

Just as financial institutions have learned to track cascade effects of financial activities on financial returns under various asset classes, they will now need to learn to track geophysical cascade effects moving through natural systems, supply chains, and the operations and priorities of their peers and rivals. Those climate-related cascade effects are reshaping underlying value already, and will be factored into overall accounting of holdings and prospects, across sectors.

In their October 2021 Communiqué, G20 Finance Ministers and Central banks recognize the importance of active investment toward the 17 United Nations Sustainable Development Goals, and are endorsing a G20 Sustainable Finance Roadmap and the Synthesis Report prepared by the Sustainable Finance Working Group (SFWG). The Roadmap treats climate and nature as critical areas of investment, and will work with international organizations and the Financial Stability Board to develop strategies for finance to reduce risk.

The Communiqué also declares:

We recognise the importance of gradually expanding the G20 Sustainable Finance Roadmap’s coverage to include additional issues, such as biodiversity and nature as well as social matters, based on mutual agreement by G20 members in the coming years.

It also calls for the IMF to create a Resilience and Sustainability Trust (RST):

to provide affordable long-term financing to help low-income countries, small developing states, and vulnerable middle- income countries to reduce risks to prospective balance of payment stability, including those stemming from pandemics and climate change.

Central banks will move toward penalizing capital flows that foster expansion of fossil fuel production. The reliability curve will be inverted—meaning the low cost of renewable energy systems, at scale, will provide a better stabilizing buffer for energy prices and supplies than the wildly fluctuating prices of fossil fuel markets, which often set prices in a way that is contrary to consumer interest or mainstream economic sustainability.

Long-term economic development strategies that depend on underlying fossil fuel revenues, or affordable supplies, must be reconsidered before it is too late. Fossil fuel dependency will be treated by international lenders, and eventually by capital markets, as a problematic form of structural indebtedness, because far more of the cost of energy than is rational or sustainable will be flowing from those markets to cartels based elsewhere.

This unnecessary leakage of capital will reduce that market’s ability to invest in innovation and secure a future of climate-smart prosperity. That leakage of capital and innovation lag, together with expanding costs from health-related, economic, and political impacts of worsening climate disruption, will increase the cost of borrowing and further undermine that market’s competitiveness.

This will seem like a very different future to many in the financial sector, because the world’s ongoing dependence on fossil fuels and the dynamics of commodity markets still provide opportunities for financial windfalls. The problem is: Those opportunities are becoming fewer and more uncertain, and this other future must and will take over; there is no viable future economic scenario in which the status quo holds.

In 1992, the nations of the world agreed to “prevent dangerous anthropogenic interference with the climate system”. In 2015, the Paris Agreement updated that framework so every nation had a role to play and a way to prosper by helping to prevent danger for everyone.

In Glasgow, next month, nearly 200 nations will gather with thousands of expert observers to significantly upgrade global ambition, with an aim to achieving that best of 5 futures examined by the IPCC. Already, $88 trillion in wealth is committing to align with that future, through the Glasgow Financial Alliance for Net Zero (GFANZ).

To ensure that best possible future plays out everywhere, we need to unblock those green capital flows at a speed never before seen. This boom economy will be far bigger than the early internet boom. New wealth creation will happen on an unprecedented scale, and should include diversified and expanded income for small farmers contributing to natural climate services.

The European Union’s planned Carbon Border Adjustment Mechanism (EU-CBAM) will create an enforcement mechanism built around global trade. To be favored in such a scenario, a trading partner needs to price carbon pollution and rapidly reduce emissions. That club of carbon pricing nations should be as big as possible, and should align policies not only through “market mechanisms”, but also through “non-market approaches”.

The COP26 likely won’t set a numerical “floor price” for carbon pricing, but it can set rules for carbon accounting, agreed emissions reduction timelines, and suggested “non-market” alignment strategies nations can use to harmonize their climate-related transitions in energy and other sectors.

Anyone who hasn’t figured out how to build the cost of carbon pollution into their business model, or eliminate carbon pollution from their business model, needs to start doing that right now. Rising carbon prices, trade restrictions, portfolio conditionalities, and other inducements to clean innovation are coming.

Capital is going to go green. The question is whether it will happen fast enough to avoid unnecessary waste and devastation.

This article is a Resilience Intel brief on the pressures facing green and yet-to-green capital, ahead of the COP26 U.N. climate change conference. Read more on related macrocritical resilience issues at ResilienceIntel.org